In previous posts, I shared some of the data we are collecting at OrthoFi. In a series of blog posts, I hope to share more of the data we have collected from over 70,000 starts and over $300,000,000 in orthodontic production. Today we discuss patient accounts receivables.

During the recession, times were not so good in metro Detroit where I practice. In fact, Detroit was going through a recession before the rest of the country experienced the banking recession. The big three automakers were downsizing in an attempt to become more streamlined, with massive layoffs and countless patients moving and transferring out of treatment and almost zero patients transferring into our office mid-treatment. It was not a great time to live in my area. Just when times were improving and the automakers had a sound plan in place and began hiring, the banking crisis hit. The car companies did not plan on the lease market evaporating due to the credit crisis and what was already a very thin turnaround margin created the much-publicized bankruptcies of GM and Chrysler and nearly bankrupted Ford.

From an orthodontist’s perspective, doing things ‘like we have always done’ would have been a recipe for my own bankruptcy. So, in order to keep our doors open, we were forced to cross our fingers and become extremely flexible both with our down payment and with how low we would allow monthly payments. This created the need for us to extend payment terms beyond the estimated treatment time. What we learned along the way shaped the way we offer financing in our office and ultimately some of how we modeled OrthoFi. We were called ‘dangerous’ and told that our financial principles were ‘a recipe for disaster’. However, we now have over $300,000,000 in orthodontic production and the corresponding payment data related to how patients actually buy and pay for treatment and are now able to cement our recommendation with data.

The industry gold standard for collections has historically been 3% patient receivables delinquency and 1-1.5% default. Additionally, the following guidelines were considered paramount to collection success:

- Extending payment terms beyond treatment length will almost certainly equal poor collections.

- You MUST get 20% down and/or cover your transaction cost (e.g. Invisalign lab fee) on each case in order to have healthy cash flow.

- 50% of ‘non-A’ patients will not pay, are not profitable, and thus should not be pursued as clients.

Personally, we had a different experience when we were forced to loosen our collections. We experienced rapid growth and a solid collection percentage, even in the face of the worst metro-Detroit economy in nearly a century. With the foundation of OrthoFi, we set out to test these principles across all markets and have discovered the previous gold standards mentioned above are outdated. In fact, in order to experience growth in a new market, a new gold standard of financial principles must be considered:

Principle 1: Offer a wide range of flexible terms, within and beyond treatment length without compromising on your collection rate:

In today’s market and economic environment, flexibility around your payment options is a must-have. Given truly open choice to customize their individual payment plan, people choose from an amazingly wide range of payment terms, most of which are outside traditional payment options. Simply allowing people to be in control of their own terms stimulates practice growth. For in-depth analysis of this topic, please see my article on the power of flexibility.

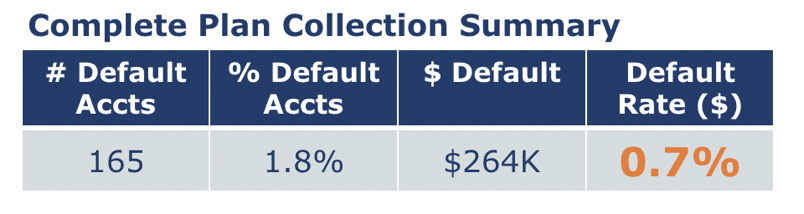

But how does that flexibility fare on the back end in terms of securing payment? OrthoFi currently manages over 40,000 individual payment plans and over $100,000,000 in patient receivables. Of that production total, 9,274 of those plans have been paid off or have reached term and should have been paid ($37,800,000 in production). The data shows the percentage of default still remains very low despite what would previously be considered ‘risky’ financial principles:

We consider payments past 120 days due as ‘default’. There is reliable data to show that some of these patients eventually do pay. However, for this discussion we are considering amounts beyond 120 day as projected default. As you can see, the default rate across a large population is something most industries would envy. In fact, the industry average is around 1.5%, and the gold standard has historically been 1%. To clarify, ‘default’ is not synonymous with ‘has paid nothing’. Also, ‘default’ does not define when in their payment plans the patient stopped paying as depicted in the following graph:

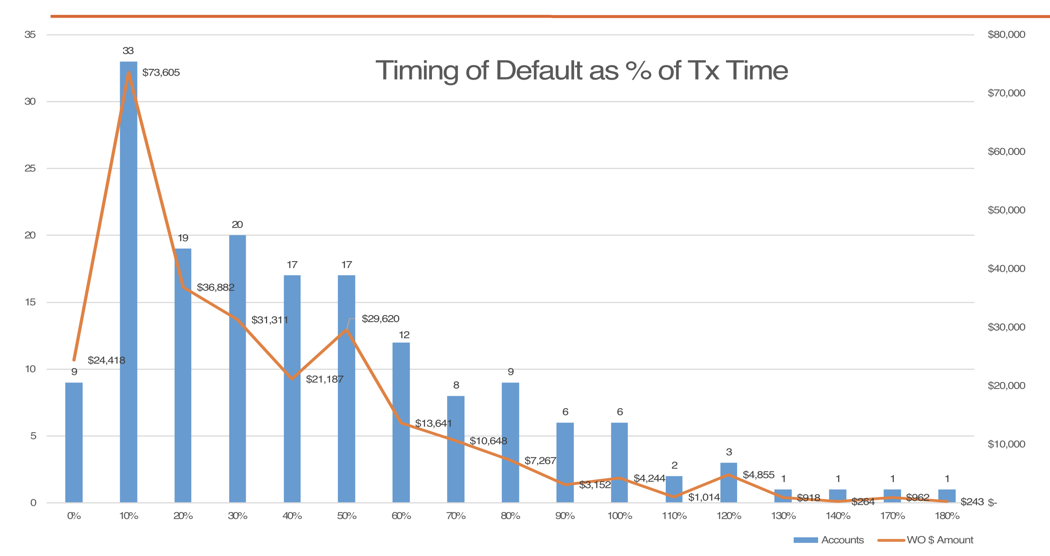

The graph above describes at what point along the payment plan the patient stops paying. The Y-axis shows the number of default plans and the X-axis shows at what percentage of the estimated treatment time the payment plan became in default. The orange line depicts the dollar amount written off at each stage of treatment. For example, if the original estimated treatment time was 18 months and they stopped paying at 9 months, the default would appear in the 50% bar above.

As you can see, almost all default – a staggering 95% – occurs WITHIN treatment time and NOT after. So the idea of limiting payment time to treatment time does not buy you much in the way of added security. It only limits your appeal. On average, $2,400 per patient was collected even when they eventually defaulted. Assuming a $5,000 average fee and a 50% operating margin, even default cases nearly break even, meaning that the average default case scenario isn’t a true loss. You just didn’t MAKE money on those exceptional few. Of course, the occasional Invisalign patient that defaults early in treatment is a loss. That’s a tough one, and unfortunately we tend to remember those. However, they are the exception and not the rule, and your financial policies should never be set around these outliers. In aggregate, the risk of that one scenario is minimal, and you cost yourself much more in realized production than you gain by protecting yourself from outliers. In fact, you will actually protect yourself from much more profitable growth.

Principle 2: Cash flow should be managed in aggregate:

It’s not necessary to cover all of your upfront costs for each individual patient if you offer open choice for your patients. A wide array of payment selections (some pick higher down payments and some pick lower down payments) creates sustainable cash flow to allow for lower down payment or lower monthly choices when needed. Using this philosophy, OrthoFi’s clients average 22% PIF and $834 average down payment for those that don’t pay-in-full. Blending those numbers yields a healthy $1,354 average Same Day Cash per case (SDC = (PIF + DP)/Starts). Applying concepts 1 and 2 in your practice will likely spur rapid growth. For detailed explanation about how to intelligently manage cash flow, please see my previous post.

Principle 3: If managed properly, higher risk plans/patients are still profitable:

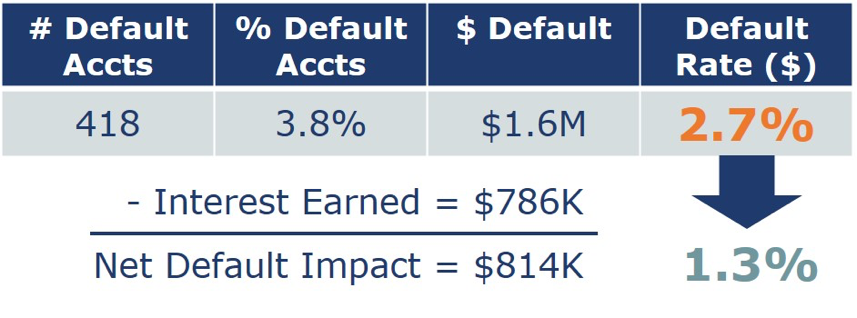

Of the nearly 40,000 active plans, 10,833 are for terms longer than 25 months ($60,800,000 in production). At first glance, their default rate is higher than shorter payment terms. However, when you consider the interest income gained from these plans, the total default is substantially decreased.

The above chart shows $1.6M gross default, which is 2.7% of the total production for that group. However, remember that OrthoFi applies a low interest rate for extended plans, designed to offset the incremental risk and splits the interest income with the practice. So when you add back the $786K interest that was earned by practices for those plans, the net default is cut nearly in half to $814K. This yields a 1.3% default for the extended plans, which gets us within the average industry default range, even for these most aggressive plans. So that’s hardly significant enough ‘risk’ to avoid treating these patients. And, when blended across all payment plans, the default percentage we see is still 0.7%, well below the previous gold standard and inclusive of the new ‘risky’ extended plans.

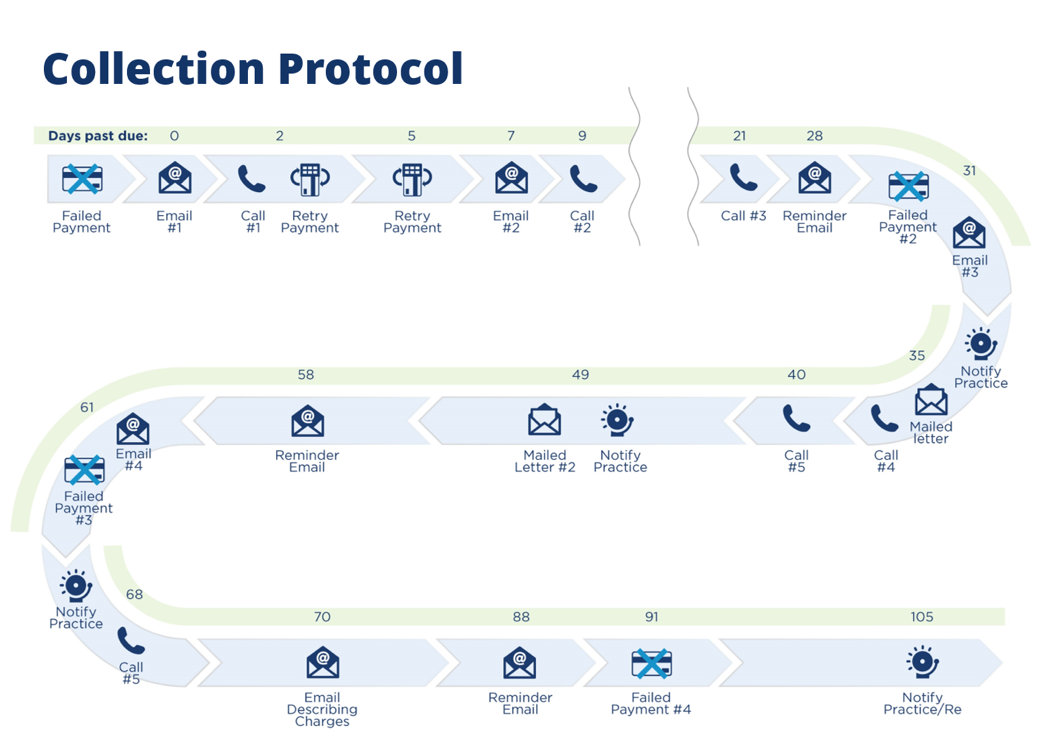

What is proper management?

The above flow chart shows the 22-step protocol we have behind our collections, by days past due for each account. Every patient is able to choose their preferred date to withdraw payment, which means we need follow-up action every day. Proper management can’t be done with batch systems, where you wait until things pile up and then make calls on the 1st and 15th or on an admin day every other week. The key is to make sure every account is touched proactively from the very start, and done consistently. Managed this way it’s possible to have 99.2% of your AR balance be current or within 10 days. The longer you wait to make a touch risks passing 30 days, when everything gets exponentially more difficult and uncomfortable. Once a patient is more than a month’s payment in arrears, getting things back on track is harder, so you need systems to make sure that you stay on top of things from day ZERO. The key here is absolute consistency in the process.This process doesn’t take vacation or sick days, it runs reliably day after day, month after month, and it’s made a world of difference in our collection numbers.

So when receivables are managed with watertight systems, collections will not be an issue. People will pay and default will remain low. When systems are managed properly, not offering flexible plans will be costing you significant dollars and not the other way around. You are the best doctor around and people belong in your office being treated by you and your talented team. Let them! Managed appropriately, it’s the best possible scenario for the patient and the doctor: win-win.

UP NEXT: Why none of this even matters…

Great article Jamie! As a consumer, fexible payment plans that go beyond treatment make sense. Happy patients pay their bills and are more likely to refer others, it truly is a win-win! Your management of receivables is so strong, but for those who don’t pay, your collection process is fantastic, go Ortho Fi!!

Thanks Mike! Process and consistency are the keys to success in many areas. Especially here.