In previous posts, I shared some of the data we are collecting at OrthoFi. In a series of blog posts, I hope to share more of the data we have collected from over 76,000 new patient exams, over 50,000 starts and over $226,000,000 in orthodontic production. Today we discuss down payments and monthly payments. There are a variety of ways to present treatment fee options. The best performing offices engage in some active negotiation with the patient over their down payments and monthly payments. However, this requires a very efficient infrastructure as well as a talented and sales-savvy treatment coordinator. As a result, rather than negotiating most offices offer two or three options for a patient to select from.

Typically the options are:

- Payment in full (with some associated discount)

- A 15-20% down payment with monthly payments that coincide with treatment time

- Perhaps a low or zero down option

- Outsourcing to 3rd party financing (e.g. Care Credit) for extended payment terms

But what if the patient were allowed to choose from a virtually unlimited number of down payment and monthly payment options and customize their plan to their individual financial needs? What do people who finance their treatment ($X down and $Y per month) choose? Also, if we are offering extended credit to all potential customers, how does credit score impact how they choose to pay for treatment? The answer lies in the data…

Across more than 50,000 starts in over 100 practices, we see an average of 22% of all patients selecting to pay in full (PIF). The typical discount we recommend for PIF is 3%, as we’ve seen that higher discounts offer diminishing returns. However, practices can customize that based on their cash flow needs. As for the rest who need financing, we use the OrthoFi slider, which allows prospective patients to design their own terms with full open choice. When we first started offering downs as low as $250 and monthlies extending out as long as 36-months, we were not sure what would happen. What do they choose? The answer lies in the data:

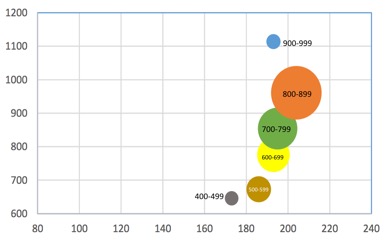

This is an interesting chart. It’s a little confusing at first glance so, let me explain. Data are grouped in bubbles representative of credit score grouping. For example, the green ‘700-799’ bubble represents the options chosen by people who have a 700-799 credit score. Bubble size indicates relative amount of people in that group. Bigger bubbles equals more people in that credit grouping. On the Y-axis is the average down payment ranging from lowest to highest. On the X-axis is the average monthly amount selected. In discussing financing options with many doctors over the years, I think an assumption most of us have is that people with good credit have more money and are able (and willing) to put more money down and pay more money per month.

Our data proves that people with better credit do, in fact, tend to put a little bit more money down. As you look at those bubbles and follow the Y-axis, people with higher credit tend to put a little bit more money down as credit score increases. However, a note to those who demand $1,500 down payments for Invisalign or other high lab fee technologies: all credit groups chose down payments with $1100 or less down with the vast majority being under $1000 down.

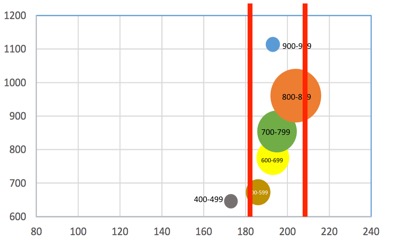

But the really interesting finding was around monthly payments. Again, you might assume that people with better credit have higher income, and thus will pay higher monthlies. However, you can see with aid of the vertical lines that all averages fall between $185 and $205 per month regardless of FICO score, except for the very small amount of people with sub-500 credit.

Higher credit did translate to higher monthly choices, but that difference was only $20/month. This shows that the price of orthodontics is not infinitely elastic – that consumers believe that orthodontics should cost $200 or less a month. If you think about it, there are a lot of families you likely know who are house/car rich and cash poor, who are overextended with private school tuition, music lessons, etc. So the truth is that no matter what technology you use or how premium your treatment might be, you need to be able to make it around $200/month, regardless of what income bracket you treat. Remember, this is validated across $226 million in orthodontic production.

So, what can we conclude from this data set? People in all walks of life, with all ranges of income and creditworthiness, want orthodontic treatment to be less than $1000 down and $200 or less per month. If you are not offering flexible options to allow for this range of payment options, you are likely letting a lot of business walk away. Also, in case you missed it, this information and a whole lot more is covered in a webinar I did for OrthoFi recently. You can find the replay here: https://vimeo.com/177147940/9e8d708da3

NEXT UP: Will people pay more in total to get more affordable monthlies?

Jamie, what is data you have on “% of people who’s payment plan is significantly longer than their treatment not paying”? Like an 18 month treatment on a 36 month payment plan? I know Ben’s thoughts on the topic (and agree with him), but was wondering if you had any data to show.

Essentially the same question. Any data on delinquency/late or non payment on 18 months of treatment and 28 months of payments, for example.

Great information and love the charts! Also would be curious to know what the delinquency rates are reversing the monthly payment amounts and down payments.

Acceledent has a few studies addressing this same question (or maybe the Accelxent rep quoted an OrthoFi study, I cannot remember). In any event, what they found was that the rate of patients not paying after their treatment time was complete was extremely low. I want to say 2-4%. From their studies they concluded that most people who are going to be delienquent will do so within the first 6 months of treatment or so, not after treatment has ended. There has to be patient education in regard to extended/flexible payment plans (i.e. total treatment fee is for the final result, not how long it takes to obtain that result, we are only extending payments past our anticipated completion date as a courtesy to make treatment as affordable as we can, etc). Not sure the validity/reliability of the Acceldent studies, but the results empirically make sense. Obviously their product is inherently back-ended in terms of cash flow so they want you to take on the risk of financing vs. passing the cost onto the patient up-front, etc.

Thanks for the comments all! I will get to the details of this in several later blog posts, but I can only speak to what we are seeing in OrthoFi. We see WIDE variety in the collections ability of individual offices before OrthoFi takes over. My office has been on the longest (will be 3 years in November) so we have yet to have one full 36-month cycle go thru. We currently sit at 99% less than 30 days delinquent. However, your collections all depends on your systems. If you don’t have reliable, always on, everyday collections processes then extending terms will get you in collections trouble very quickly. If you have reliable systems, 99%+ will pay. In 2015, OrthoFi managed approximately $55M in patient A/R and had a default of 0.42%. Also, the breakdown on that default is not just the extended terms as you think. So called ‘A’ patients who choose short plans default too . Also, as you will see in my next post, we recommend charging a small (2.9-6.9%) finance fee on extended plans. So, interest income minus default puts you over 100% collections. Not bad. But, systems have to be dialed in to have great flexibility. You need both!

Great article! I am actually in the process of implementing Orthofi for one of our offices in Oregon. The biggest concern for the Doctor is extending payments beyond treatment time. Adding a nominal finance fee is very appealing. Offering flexibility with down/monthly without any preconceived ideas on a patients ability to pay is integral to increasing case acceptance in a practice.

Agreed Tuesday! Rather than erect an insurmountable wall in front of your practice by charging large down payments to manage risk, why not do what everyone else does and charge interest? And, we have nearly 3 years of collections data that shows, when managed properly, delinquency risk is not a concern. Will have much more on this in the coming months when I cover the collections data in detail.

ps. I have checked out your blog and you guys seem super sharp. Nice job!