In previous posts, I shared some of the data we are collecting at OrthoFi. In a series of blog posts, I hope to share more of the data collected from over 75,000 starts and over $300,000,000 in orthodontic production. Today we discuss why the approach we have historically taken to sales strategy and the impact it has on receivables is dumb. Over the last year, I have posted a sequence of data-driven blogs describing how you should focus on Same Day Starts, and how you can be ultra-flexible with your financial terms and still maintain healthy aggregate cash flow to pay your bills while your practice grows. The most frequent question I receive is ‘flexible financing seems great, but do people actually pay?’ Seems like a perfectly legitimate question considering how we have historically been taught to think about financing risk, so I posted a blog with hard data on over $100M of receivables, and showed that when practices are managed with the requisite watertight systems in place, you can get the best of both worlds.

Why is it so hard for us to accept that? Well, our short-sighted and hyper-detail oriented mindset inevitably focuses on that one patient two years ago who screwed us on our Invisalign lab bill. That one insidious thought has led to a specialty-wide brain fart on how to treat prospective patients, and, in the process, has likely fueled the rapid growth of corporate DSO orthodontics. DSOs are run by people with big-business experience, who have long known about our so-called ‘novel’ approach to patient financing.

Frankly, in retrospect, we (myself included) have been very, very dumb about most of this stuff. Although the hard data should be enough proof that flexibility can still come with good collections, the truth is that none of that even really matters, considering a little thing called VCM. Let me explain:

First, let’s define the two basic types of costs we experience in an orthodontic practice:

- Fixed Costs: These are costs associated with running a business that do not change with units produced. Rent, office salaries, utilities, cable, etc are all stable or relatively stable regardless of the amount of patients you start. If you experience significant growth, it will be necessary to add fixed costs by hiring another employee or moving to a bigger space, however these costs do not change on a start-by-start basis. Your phone bill does not go up or down if you start a new patient.

- Variable Costs: These costs vary directly with how many patients you start. If you start another Invisalign case, you owe another lab bill plus glue for the attachments, the little bag you might pass out the aligners in, extra tray covers, and maybe swag you give to each new start. These costs exist when someone starts and do not exist if someone does not start.

For basic accounting purposes: Fixed Costs + Variable Costs = Practice Overhead.

When considering fixed vs variable costs, typically, in an orthodontic practice, the amount you spend each month on fixed costs is much larger than your variable costs. In any orthodontic office, the largest expense involves payroll. Once payroll and other overhead is paid, the remainder of the expenses are only related to the expenses specific to each patient starting.

For example, let’s consider an office with 60% overhead expense and an average treatment fee of $5000. Even if we used ‘expensive’ braces and wires, etc the incremental cost is still relatively low making the remaining expense in the fixed category:

Variable Cost: Self-ligating braces, adhesive, wires, and patient perks: $700 (14%)

Fixed Cost: Rent, salaries, phone, cable, lawn care, computers, etc: $2300 (46%)

At a certain point your fixed costs are paid for, but your capacity to treat additional patients remains open. So, once you hit a certain amount of production (specific to each practice), you essentially have no more fixed costs to pay when you start an additional patient. All revenue above that is subject to Variable Contribution Margin (VCM).

That carries until you reach the volume where you need to hire additional staff or grow your footprint. Typically, practices have up to 20% open capacity, so you can treat that many more patients while only incurring variable costs. Using the above cost breakdown, each additional patient costs only $700, yielding an 86% VCM. Even your Invisalign cases are around 70% VCM. As you can see, patients you treat ‘on top of’ your existing volume are extremely profitable.

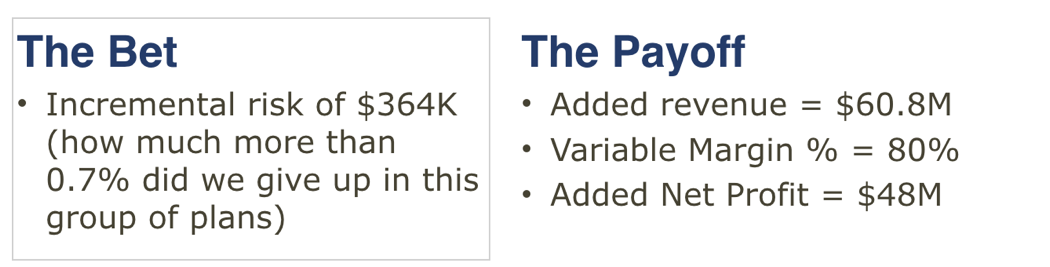

With that fact in mind, let’s revisit collections and receivables data. For the sake of argument, let’s assume that, if you implemented our recommended flexible financing approach, you would only grow by the amount of people who would choose riskier extended plans. Of the nearly 40,000 active plans, 10,833 are for terms longer than 25 months ($60,800,000 in production).

Let’s imagine OrthoFi and the collective data as one big practice (instead of many small practices). It is safe to assume most of the $60.8M of production for extended plans was incremental – starts most practices would not have gotten with more traditional higher-down and fixed month terms.

- My last post detailed the net default impact % for plans over 25 months = 1.3%

- It also explained the overall rate of default across all plans = 0.7%

- So, the increased default risk from extended vs overall plans is 1.3% – 0.7% = 0.6%.

- Multiplying the $60,800,000 times the increased risk of 0.6% yields a comparatively low number: 60,800,000 x 0.6% = $364,800.

What does this mean? It means that, the business gained $60.8M in additional revenue by risking an additional $364K in default. Now, considering this revenue stream was likely incremental (i.e. revenue gained on top of standard revenue and subject to incremental costs only (fixed costs have already been paid by your other production). Assuming an 80% incremental margin (conservatively assumes a 38% Invisalign mix in your practice), the $364K in risk gained an extra $48M in profit.

Not a bad bet, eh? Making the math small again to relate to an individual practice, let’s subtract a couple decimal points off the above numbers. Would you take an additional $480,000 if it meant risking an additional $3,640 of it, leaving you with $476,360 in net profit? Of course you would! Even if my math was off by 500%, would you risk $3,640 for $95,272? Anyone would make that bet all day long and twice on Sundays. Again, as the name of this post implies, the math makes our previous concerns about default rate seem relatively dumb.

So the moral here, if you have followed along with the math, is that adding incremental starts by becoming flexible with your plans, even if they are ‘riskier’ plans, is likely the smartest and most lucrative thing you could possibly do for your business. Not to mention the social obligation to provide excellent care to those who can’t afford traditional terms. Win-win situations are the best! [*mic drop*]

Mic drop indeed! Excellent!

Best explanation ever on why this makes sense. L