In previous posts, I shared data we are collecting at OrthoFi. In a series of upcoming blog posts, I hope to share more of the data we have collected from over 76,000 new patient exams with over $226,000,000 and counting in orthodontic production. Today we discuss: will people pay interest on orthodontic treatment fees?

There has been a lot of discussion in recent years about extending payment terms to help make treatment more affordable. In my practice, we started extending terms during the ‘Great Recession’. I live in Detroit and times were not good. We didn’t want to extend terms, but it was either change and be more flexible or don’t survive. We chose to live to fight another day. However, extending terms can cause cash flow issues if you aren’t careful as well as increase the default risk to the orthodontist. We have been told for years that the antidote for ‘risky’ patients was to jack the down payments up and raise monthlies thereby ‘protecting’ us from risk. At the same time, however, we ran off countless good patients who simply couldn’t afford our terms. We hypothesized that, instead, we should do what every other business does (companies which are much more business savvy than orthodontists by the way): charge interest to hedge the risk of extending payments. But, would orthodontic patients pay interest for their treatment? Many thought no. We believed that a certain percentage of patients pay interest for pretty much everything they buy, so why would orthodontics be any different. Here’s what the data showed:

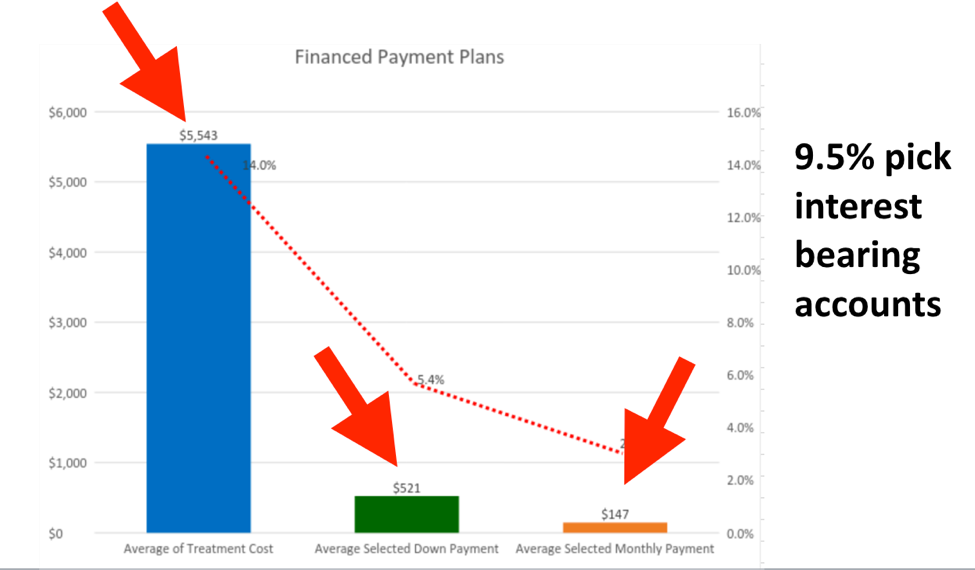

We found 9.5% of all patients (remember this is across $225M of production so not a small sample) will pay interest. In some offices, the percent of patients who choose interest bearing accounts is near 15% of all starts.

The graph above shows three columns. On the left denotes the average fee patients who choose interest bearing plans pay: $5543. Interestingly, this fee is almost $288 higher than the average fee per start across OrthoFi: $5254. The middle column shows the average down payment selected by patients choosing interest: $521. This is over $300 less than the average down payment of $834. Also of note, the system will allow for a $0 down payment, so the people who choose interest bearing accounts are still making down payments. The final column shows the average monthly payment selected by patients who chose interest bearing plans: $147.

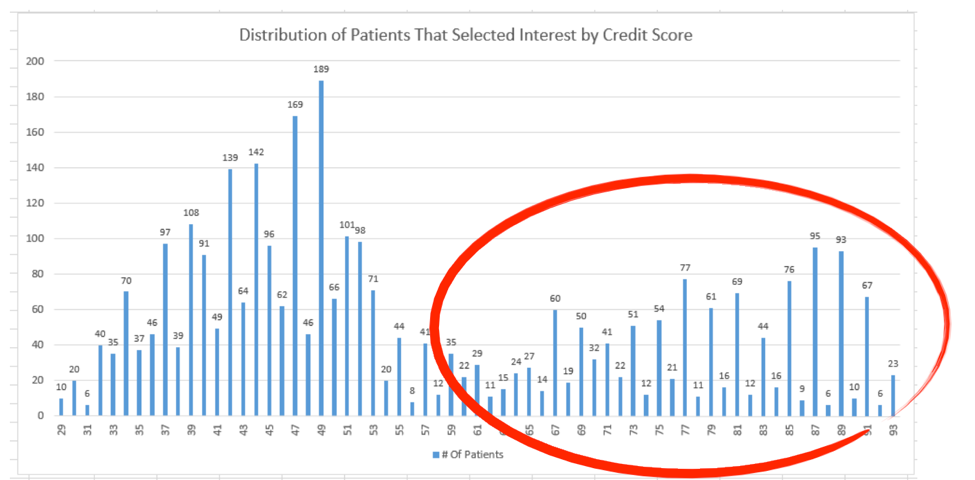

Also, I think most people–including us–anticipated only the ‘risky’ patients would choose interest bearing plans. So we wanted to look at the distribution of people selecting interest bearing plans for each credit score. Here’s what we found:

The graph above shows the amount of people selecting interest on vertical axis and the credit score on the horizontal axis. The further to the right on the graph, the better the credit score. What we found to be very interesting is that, although the distribution of people selecting interest is highest in people with lower credit scores, there is still a very significant portion of people selecting interest-bearing plans who also have good or very good credit. Of note, the highest interest rate charged through OrthoFi is 6.9% with most plans under 5% interest. Interest terms are calculated based on a proprietary credit algorithm and the length of payment terms. Many people wonder why the rate isn’t above 20%, similar to credit cards or other lending services. The reason is that lenders typically make money off lending money and therefore need to charge much larger interest rates to cover their risk. Orthodontist make money by doing orthodontics, so the risk is much lower. We only need to charge interest at a rate to cover our default risk, which is very, very low.

So, what conclusions can we make from this data? First, people will willingly pay you more total money for treatment if you allow them to make a lower down payment and a lower monthly payment. Second, about 10% of all patients need a monthly payment of $150 in order to afford orthodontic treatment. Third, a meaningful number of the patients who do need the lower payments and extended terms have good or very good credit. Good credit and ‘can afford more than $150 per month’ are not always linked as many might assume. And, our collections data shows 99.95% of all patients processed through the system to date don’t default (more on this in future posts). So, managing risk by using interest–rather than prohibitive down payments or monthly payments–is smart and valuable, both in terms of interest income and, much more importantly, in orthodontic case starts.

Also, in case you missed it, this information and a whole lot more is covered in a webinar I did for OrthoFi recently. You can find the replay here.

Up next: How to frame your messaging in the TC room.