In previous posts, I shared some of the data we are collecting at OrthoFi. In a series of blog posts, I hope to share more of the data we have collected from over 70,000 starts and over $300,000,000 in orthodontic production. Today we define receivables terms and how to calculate them.

One question we get quite often is how to properly calculate receivables. Additionally, we get questions generated from confusion created by people who are improperly calculating receivables. Most of us (myself included) had little to no training in this stuff and have to learn as we go. Today’s post will briefly define key terms, provide a summary of how we perform receivables calculations, and clarify what metrics you should be looking at to expertly manage your receivables. This can be pretty dry stuff but is necessary both for orthodontists to properly manage their businesses, and in anticipation of my next post which will focus on the receivables data we have gathered.

Same Day Cash: A combination of payments received at the beginning of treatment from down payments and from patients who pay in full. It is important to monitor this ratio as the Same Day Cash percentage will be what allows you to manage your cash flow while still allowing patients the choice of flexible payment terms. SDC = DP + PIF. For more detail, please see my previous post on managing cash flow (http://orthopundit.com/cash-flow-management-the-data/).

Receivable: Investopedia defines receivables as ‘an asset designation applicable to all debts, unsettled transactions or other monetary obligations owed to a company by its debtors or customers’. Receivables are recorded by a company’s accountants and reported on the balance sheet, and they include all debts owed to the company, even if the debts are not currently due. In orthodontics, monies owed after Same Day Cash is collected are a blend of ‘accounts receivable and ‘contracts receivable’ – although we typically (and errantly) define our receivables only as ‘accounts receivable’.

Account Receivable/Billed Contracts Receivable: Refers to the outstanding invoices a company has or the money the company is owed from its clients. The phrase refers to accounts a business has a right to receive because it has delivered a product or service. In orthodontics, this refers to the treatment you have completed or appliance you have delivered but has not yet been paid for. For example, when you deliver someone a new retainer who has not yet paid you for it. Or, similarly, when you have completed a percentage of treatment and have not yet been equitably paid for that percentage of treatment. These circumstances would be ‘accounts receivable’.

Contract Receivable/Unbilled Contracts Receivable: Amounts expected to be realized in future periods. In orthodontics, we typically bill for services before they are performed. Therefore, any portion of treatment that is yet to be done and yet to be paid for would be a contract receivable. Even though typical discussions regard ‘accounts receivable’, orthodontists have historically operated with very few true accounts receivable as we have been advised to never take the braces off before patients have fully paid their account. Our process is different than a furniture store which will finance, sell, and deliver a couch many months/years before the couch is fully paid for. It is our advice that – in order to remain competitive in today’s marketplace – orthodontists become more flexible in our financial policies and, when necessary, extend terms to patients beyond their treatment time to allow lower monthly and down payments to those who need them, which would increase the amount of true accounts receivable we manage. In orthodontics, since we do not ask all patients to pay in full, there are two receivables we need to actively and separately manage: Patient and Insurance receivables.

- Patient Receivables: The total uncollected dollars owed to the practice by the patient (excluding insurance) which are created because we offer people the ability to make monthly payments. Patient Receivables = Production – SDC – Insurance Receivables.

- Insurance Receivables: The second type of receivable needing active management are the total uncollected dollars owed to the practice by the patient via their insurance. There are a shocking number of times that insurance companies fail to pay as scheduled requiring active and diligent monitoring of insurance receivables due by your team. Management discussions in orthodontics typically revolve around Patient Receivables however is is very common to have a high delinquency of Insurance Receivables as well. Insurance companies much prefer insurance dollars to be in their bank accounts and not ours. Our advice is to accept assignment of insurance benefits and manage these receivables on behalf of the patient. Not accepting assignment of benefit is tantamount to ‘not taking my insurance’ in many patient’s eyes and will give your competitors who do accept assignment of benefit a competitive edge over your practice. Insurance Receivables = Production – SDC – Patient Receivables.

30/60/90: Receivables are typically looked at by what is called an ‘aging’ report. This means how ‘old’ are the receivables, or, how long has the patient owed money that they have not paid. Accounts under 30 days delinquent are typically not considered in a delinquency calculation as the industry standard delinquency calculation considers only monies more than 30 days delinquent. As an account ages, it becomes less likely to convert the account from a receivable to cash (i.e. less likely you will get paid).

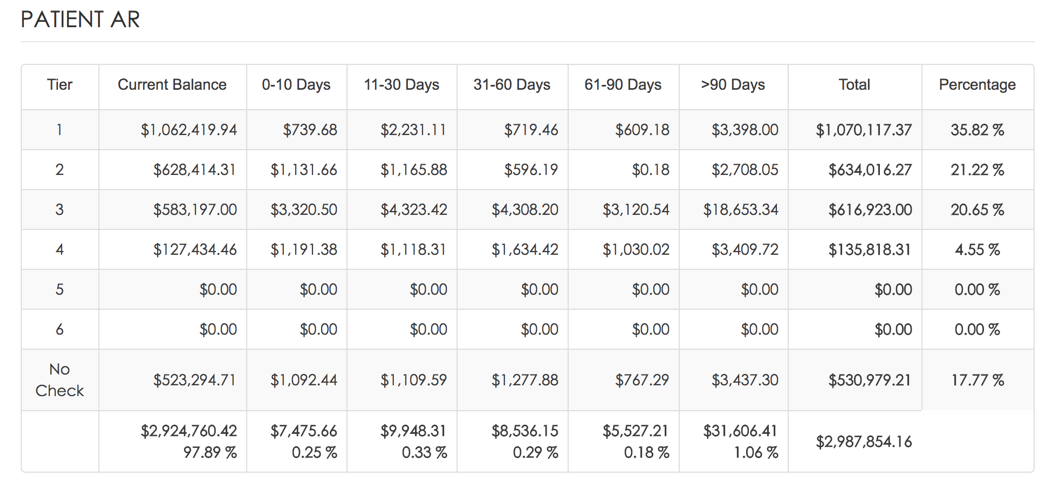

Delinquency: Percentage of total account receivables that is 30+ days past due. This should also broken into separate numbers for the patient side and the insurance side. The chart below represents how we visualize the total Patient Receivables. ‘Tier’ represents the credit rating we assign them based on OrthoFi’s proprietary algorithm. There are some patients who opt out of a credit check and are represented in the ‘no check’ group. We will dive into analysis of collections data in the following post. As stated above, receivables less than 30 days delinquent are typically not considered in delinquency percentages. Historically, an excellent collections process would be represented by a delinquency of less than 3%.

So, as represented in the above ageing report, this practice would have 1.53% patient receivable delinquency (0.29%+0.18%+1.06%).

Default: Calculating default percent is an area we see offices frequently miscalculate. Default is defined as the percent of total net production that is uncollectable. OrthoFi considers any delinquencies past 120 days as ‘uncollectable’ and thereby in default according to our calculations. They do, however, continue to attempt collections for these monies (and recommend you do as well), and do sometimes collect, but monies owed longer than 120 days have a low likelihood of collection and belong in your ‘default’ calculations. The mistake we frequently see is to calculate default rate from the AR total instead of Net Production. Default rate, or its converse collections rate, is the total aggregate amount or percentage you get from what you produce, and is not calculated from the receivables number. Default Rate = Monies due past 120 days / Net Production.

Understanding the above terms is necessary in order to understand and manage your practice finances. As increased flexibility in payment terms becomes more and more important in practice success, understand and managing your receivables is paramount to avoid unnecessary delinquency and default.

UP NEXT: Patient Receivables – the Data!